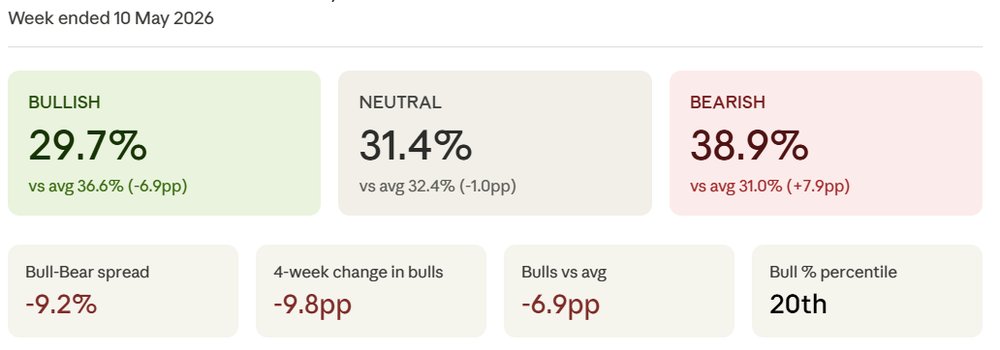

Investor Sentiment Survey

Bullish sentiment has continued to decline for four consecutive weeks, falling from 39.5% for the week ended 12 April to 29.7% this week. Investors are increasingly cautious about the future of the Australian stock market. When asked about their expectations for the next three months, many are uncertain, with options including bullish, neutral, or bearish outlooks.

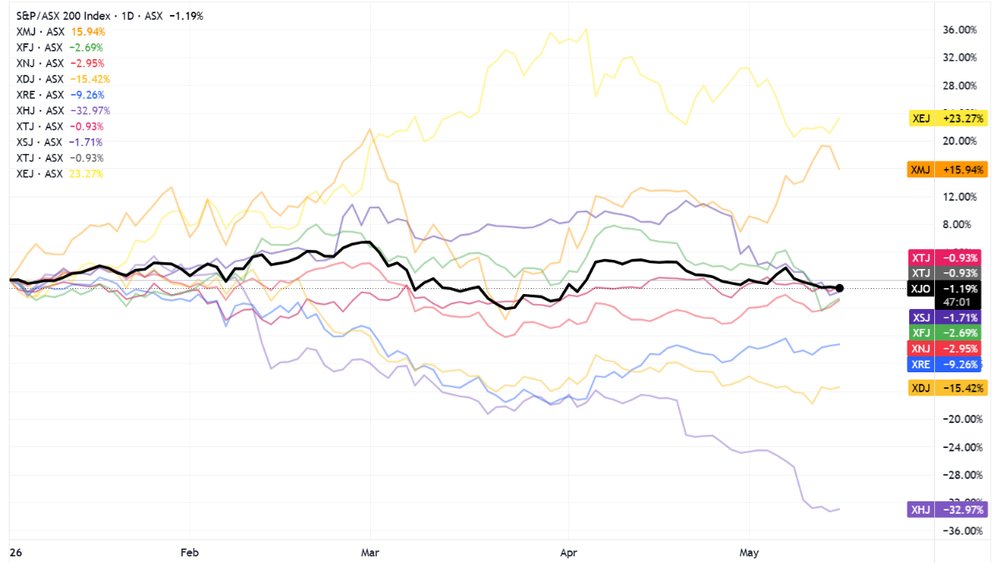

Miners vs. the World

The ASX 200 has only dropped by 1.2% for the year, but many investors feel it should be down by 10-15%. This discrepancy is largely due to the performance of the mining sector. Materials make up approximately 27% of the index, and without the contributions from BHP, Rio Tinto, and Fortescue, the overall index would likely be significantly lower.

Energy is the best-performing sector of the year, but it only accounts for around 3% of the index. This highlights how heavily the index is influenced by the mining industry.

BHP at All-Time Highs

BHP has reached three consecutive all-time highs this week, breaking through the $60 level for the first time in its history. Copper has also hit a new record high of US$6.6 per pound, while iron ore remains steady around US$110 per tonne.

Charlie Aitken from Regal has provided some insightful commentary on the commodity market. He believes that the combination of AI hyperscaler capital expenditure, defense spending, and the devaluation of the US dollar, along with a lack of supply response, sets the stage for an extended commodity price super cycle.

Aitken suggests that the best way to capitalize on this trend is to remain underweight on highly leveraged domestic mortgage banks and overweight on resources. He notes that if current commodity prices hold, BHP could generate double the current consensus estimate for free cash flow over the next five years.

CBA’s Worst Selloff on Record

CBA experienced its worst one-day selloff since its listing in 1992, dropping by 10.4% on Wednesday. This decline was worse than the pandemic (down 10.0% on 16 March 2020) and the Global Financial Crisis (down 9.0% on 18 December 2008).

The selloff was triggered by CBA’s Q3 results, which fell short of expectations due to flat revenue growth and increased provisions related to macroeconomic headwinds. The bank’s CET1 ratio dropped by 70 basis points to 11.6%, raising concerns about capital adequacy and limiting potential shareholder returns. The federal budget may have also played a role in prompting long-term shareholders to sell.

Unlike previous major downturns, this one lacks a clear crisis-level catalyst. However, with no capital gains tax relief, minimal earnings growth, property market challenges, and an elevated valuation, this could signal the start of a prolonged de-rating for CBA.

Bapcor Oblivion

Bapcor has already fallen by 67% year-to-date, following a significant dilutive share raise in February at a 65% discount. On Thursday, the company issued another earnings downgrade, further worsening its situation.

Key highlights from the announcement include:

– FY26 underlying EBITDA (pre-AASB16) reduced to $62-68m, down from the previous estimate of $74-79m, representing a 15% reduction at the midpoint.

– “Softer trading conditions in April continuing through to the end of FY26 driven by lower business confidence and consumer sentiment.”

– Current conditions may lead to a non-cash impairment, which will be assessed at the financial year-end.

Bapcor closed the session down 18.5%, and fell an additional 4% on Friday. Its year-to-date performance now stands at -76%.

Last week, several retailers, including Accent, Endeavour, JB Hi-Fi, and Super Retail Group, indicated that late March marked a clear turning point in their trading conditions. It is intriguing to see more companies follow suit with similar messages.

Last Laughs

For those seeking free investment tools and ASX research, Market Index offers a range of valuable resources. These include:

Broker consensus

ASX announcement data

Dividend information

And much more.

Access these tools and more for free at Market Index.

{kind=link}