The Shadowy Realm of Private Credit: A Looming Financial Unknown

The global financial landscape is increasingly being shaped by a sector known as private credit – a complex web of lending that operates largely outside traditional banking systems. While offering significant funding opportunities, its opacity and rapid growth are raising alarms among regulators and financial experts, who fear it could harbour systemic risks reminiscent of past financial crises.

A recent report from the UK House of Lords Financial Regulation Committee, titled Unknown Unknowns, has brought these concerns to the forefront. The 66-page analysis, developed with input from the Bank of England and the Treasury, concluded that there is “insufficient data to determine whether the private credit market poses systemic risks. It is truly an unknown unknown. Even the Treasury cannot fully grasp the risks.” The committee issued a stark warning: “Have the memories of the global financial crisis faded? Vigilance must not wane.”

Private credit refers to loans provided by non-bank financial institutions, such as private equity firms, hedge funds, and specialized credit funds, to companies. This type of financing is often sought by businesses that may have difficulty accessing capital through conventional channels like bank loans or corporate bonds, perhaps due to lower credit ratings or having already exhausted traditional avenues.

Patrick Corrigan, a professor at the University of Notre Dame Law School and an expert in financial regulation, described the situation in a recent interview. He noted that the UK report’s title, Unknown Unknowns, perfectly encapsulates the reality of the private credit market. “Information on private credit is excessively obscured—almost intentionally misleading to evade financial regulations and disclosure obligations,” Corrigan stated. “Currently, it’s nearly impossible to fully understand the entire private credit market.”

The concerns surrounding private credit have been echoed by prominent figures in the financial world. David Solomon, CEO of Goldman Sachs, issued a warning about its latent dangers in his annual shareholder letter. Simultaneously, reports emerged indicating that major financial institutions, including Blackstone, Morgan Stanley, and BlackRock, were experiencing a surge in early redemption requests from investors in their private credit funds. In South Korea, Kim Yong-beom, Cheong Wa Dae Policy Chief, reflected on the 1999 foreign exchange crisis, drawing parallels to current market instability and questioning the prevailing “AI bubble theory.”

To shed light on this burgeoning and enigmatic sector, a comprehensive examination of private credit, its mechanics, and the unfolding events surrounding it has been undertaken, drawing insights from economic, legal, and international institutional experts.

Entanglement of “Too-Big-To-Fail” Banks

A critical concern is the increasing involvement of large, systemically important banks in the private credit market. Professor Corrigan elaborated on this point: “Originally, even if private funds like private credit funds fail due to poor investments, the risk to the financial system should be minimal—individual investors bear their own losses. However, if banks deemed too-big-to-fail and eligible for public bailouts get involved, the story changes completely.”

He explained that banks, driven by a desire for higher profits in a low-interest rate environment, are actively seeking opportunities beyond traditional lending margins. “Banks dissatisfied with the spread between deposit and loan rates have an inherent drive to expand operations to the limits of regulation for additional profits,” Corrigan said. “When large banks’ funds become intertwined across sectors, risks can spread systemically—a scenario private credit now embodies.”

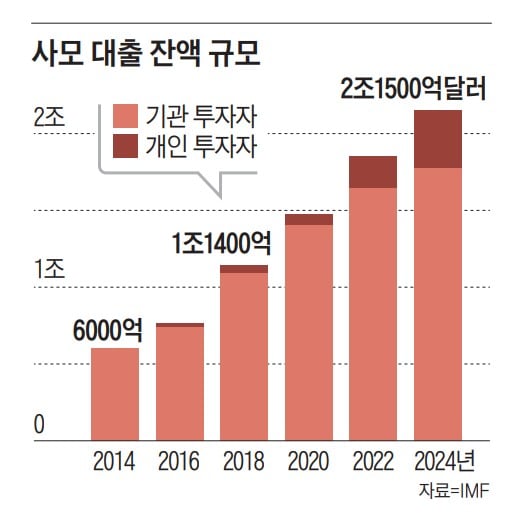

The scale of the private credit market is substantial and has grown exponentially. The International Monetary Fund (IMF) estimates its global value at approximately $2.15 trillion, having quadrupled over the past decade. This surge is attributed to several factors:

* Post-2008 Banking Regulations: Stricter regulations on traditional banks pushed some lending activities into less regulated private channels.

* Funding Needs for AI Infrastructure: The burgeoning artificial intelligence sector requires massive capital investment, much of which is being sourced through private credit.

* Investor Demand for Yield: In an environment of low interest rates, investors are seeking higher returns, making private credit an attractive, albeit riskier, option.

Corrigan highlighted how banks, while not always directly holding private credit assets on their balance sheets, are effectively funding them through less regulated affiliates like insurers and asset managers. “Though banks effectively fund private credit, multi-layered structures often obscure this on their balance sheets,” he noted. Furthermore, significant capital is reportedly flowing into private credit from retirement funds and pension funds seeking diversification and higher returns.

The exact exposure of banks to private credit remains an “unknown,” as comprehensive data is lacking. A commonly referenced indicator is the Federal Reserve’s data on loans made by US banks to non-bank financial institutions (NBFI). This metric shows a dramatic increase, with NBFI loans growing from $322.5 billion in early 2015 to an estimated $1.8 trillion by late 2024, marking an 80% surge in the past year alone.

Amit Seru, a professor at the Stanford Graduate School of Business, warned about the potential contagion effects. “If a crisis triggers widespread asset devaluation, liquidity droughts, or forced asset sales due to maturity mismatches, risks could cascade across banks, insurers, and beyond,” Seru explained. “The danger lies not in private credit funds themselves but in the complex, interconnected structures they’ve formed.”

The AI Connection: A Double-Edged Sword

The term “AI” has become ubiquitous in discussions about private credit, influencing the sector in two significant ways: the enormous funding requirements of AI development and the potential financial distress of software companies facing AI-driven disruption.

According to the Bank for International Settlements (BIS), private credit extended to AI companies has skyrocketed from $3 billion in 2015 to an estimated $200 billion by late 2024. The BIS analysis reveals that major technology firms, often termed “hyperscalers” like Google and Amazon, are financing AI infrastructure through special-purpose entities (SPEs). These SPEs typically have minimal equity and enter into long-term leases, thereby keeping the associated loans off their corporate balance sheets. Repayments are channelled through lease fees to private credit investors, often with implicit or explicit guarantees from the hyperscalers to enhance creditworthiness.

Egemen Eren, a senior researcher at the BIS, noted in a recent report that this structure facilitates substantial private credit flows into AI infrastructure, deepening the interconnections between banks, Big Tech companies, and investment funds. “If even one hyperscaler faces setbacks, overinvestment losses could spill into the banking sector,” Eren cautioned. Projections from Morgan Stanley suggest that AI infrastructure spending could reach $3 trillion by 2028, with a significant portion likely to be financed through private credit.

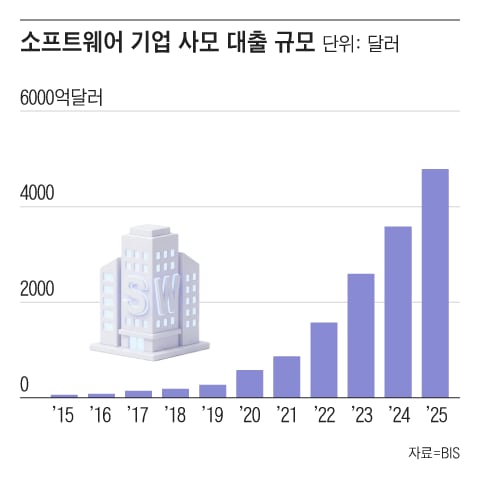

Another area of concern is the software-as-a-service (SaaS) sector. As AI technologies advance, they pose a potential threat to existing software solutions, raising questions about the financial stability of SaaS companies burdened by substantial private credit debts. BIS data indicates that private credit extended to software firms has surged from $7.6 billion a decade ago to approximately $538.9 billion by late 2024, a nearly 70-fold increase. Approximately 20% of private credit funds reportedly have exposure to the SaaS sector. An anonymous official from an international institution remarked, “Last year, private credit risks were blamed on isolated fraud. Now, it’s seen as intertwined with AI and software—a shared fate.”

The Illusion of Diversification and Hidden Risks

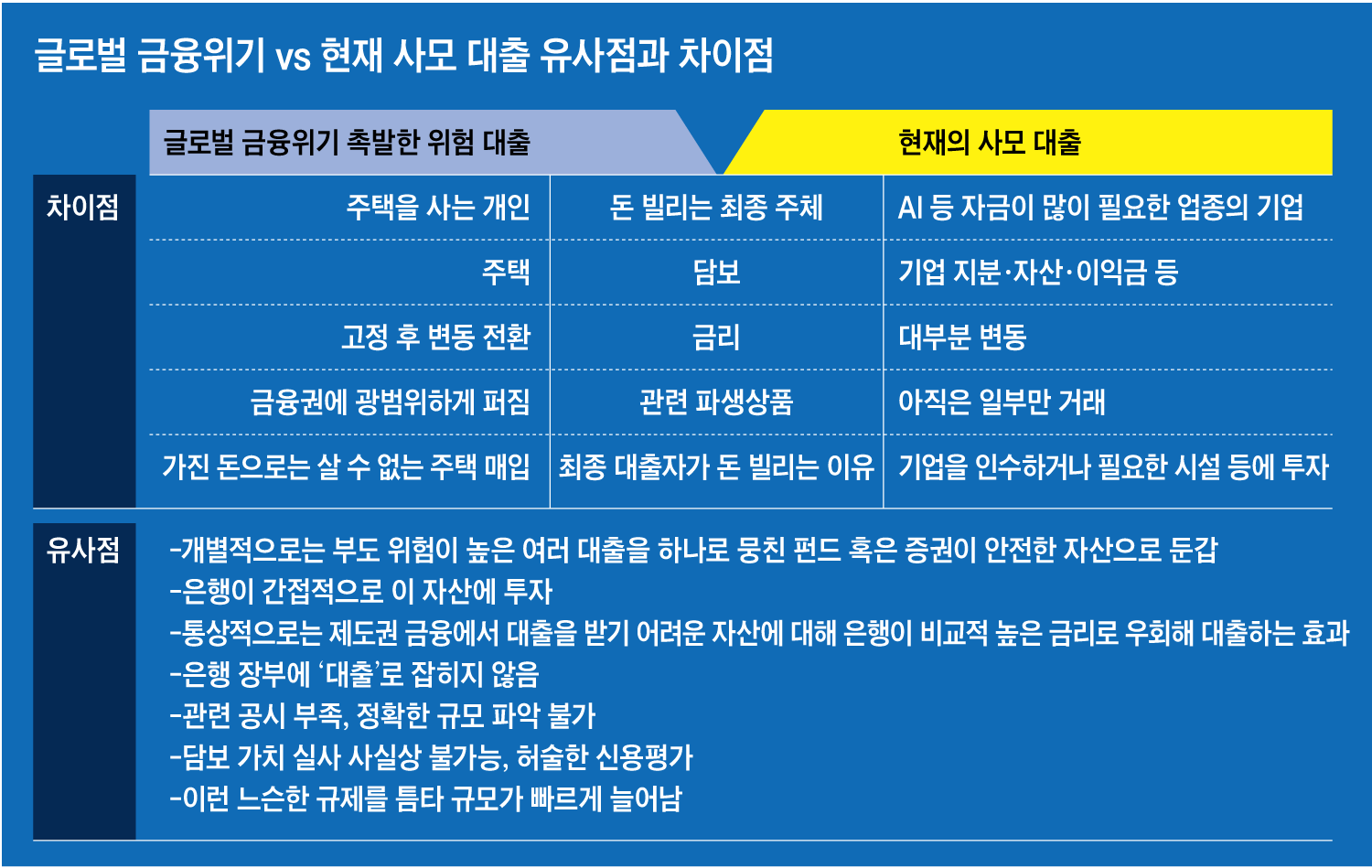

The structure of private credit bears some resemblance to the complex financial instruments that preceded the 2008 global financial crisis. In 2008, the crisis was exacerbated by investments in collateralized debt obligations (CDOs) backed by subprime mortgages. These instruments bundled risky loans into securities that were often assigned high credit ratings, creating a false sense of security. When defaults began to cascade, the underlying risks were exposed, leading to widespread financial turmoil.

Some experts draw parallels between the current private credit market and the pre-2008 environment. They point to the embedding of bank funds within private credit layers, the use of complex securities to inflate credit ratings, and a potential neglect of risks driven by profit motives. Collateralized loan obligations (CLOs), which are prevalent in private credit, are often viewed as similar to CDOs, creating an “illusion of diversification.”

Corrigan explained this concern: “Like pre-2008, CLO risks are hidden until a crisis exposes them.” He identified a potential trigger point: unused credit lines that banks have committed to private funds. His analysis revealed that US banks’ uncommitted NBFI credit lines had reached a staggering $928 billion by late 2024, representing a 575% increase over 15 years. “A crisis could force funds to draw these lines simultaneously, overwhelming banks with nearly $1 trillion in sudden liabilities,” he warned.

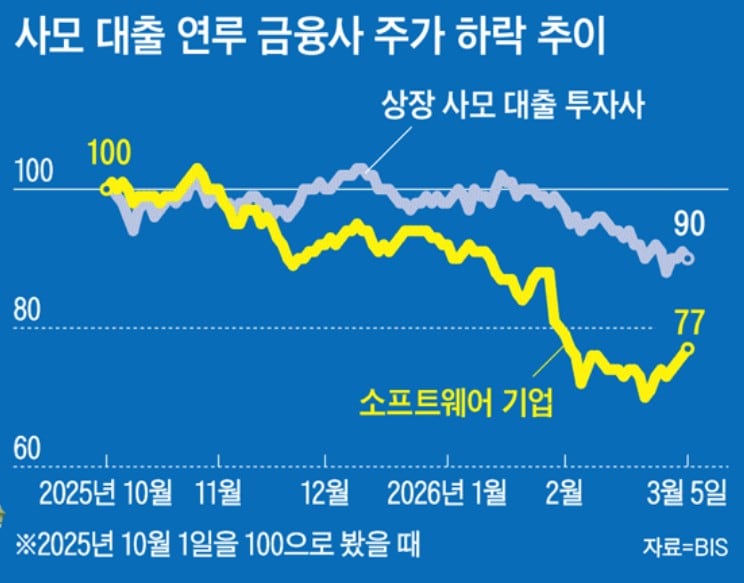

Beyond CLOs, other risk factors are emerging. These include “pay-in-kind” (PIK) clauses, which allow interest payments to be added to the principal, increasing the loan amount over time, and partial redemption rights, which can potentially trigger fund runs. Bloomberg reported that 12% of private credit arrangements included PIK terms in the second quarter of 2024. The recent difficulties faced by Blue Owl Capital, which halted quarterly redemptions amid fears of an AI-driven software market downturn and a spike in withdrawal requests, serve as a cautionary example of these risks.

However, not all experts anticipate a crisis of the magnitude seen in 2008. Bobbie Reddy, a professor of law at Cambridge University, offered a more tempered view, stating, “Most banks have controlled private credit risks, making a systemic collapse unlikely.”

Calls for Transparency and Global Investment

Across the spectrum of expert opinions, there is a consensus on the urgent need for greater transparency in the private credit market. Reddy emphasized this point, noting the challenges in achieving it. “The US SEC’s 2022 attempt to mandate private credit fund disclosures was blocked by courts as ‘overregulation.’ Yet, given the market’s growth, transparency on asset valuations, fund structures, and risks is critical,” she stated.

In South Korea, pension funds and institutional investors are increasingly allocating capital to private credit as an alternative asset class. These entities are reportedly conducting thorough risk analyses. According to the Financial Supervisory Service, the total balance of overseas private credit fund investments facilitated through securities firms amounts to $14.5 billion. Notably, the National Pension Service and the Korea Investment Corporation (a sovereign wealth fund) have made substantial investments, reportedly around $8.8 billion and $4.8 billion, respectively, into these markets. The growing involvement of these large investors underscores the global reach and significance of private credit, further emphasizing the need for enhanced understanding and oversight.

{kind=link}